Table 2. Source: StatsSA General Household Survey 2018, LCS 2015, TransUnion Financial Hardship

COUNTRY IMPRESSION

SOUTH AFRICA

VALUE CHAIN SOLUTIONS (VCS) HAS HAD THE OPPORTUNITY TO WORK EXTENSIVELY IN THE SOUTH AFRICAN FOOD AND BEVERAGE SECTORS.

With the outbreak of COVID-19, the economy has seen drastic adjustments, the effects of which are still unfolding. Currently consumers and businesses are faced with extreme uncertainty and volatility, placing pressure on all to adapt and adjust on a constant basis.

In conjunction, South Africa is experiencing a very wet crop production season which may result in significant surplus grain and oilseed stocks. However, in spite of a surplus scenario becoming more likely, grain and oilseed prices are at historical highs given global commodity market developments. This creates significant raw material cost pressures in almost all food and beverage value chains, including the fresh and processed meat value chains. Consequently, end-consumer product prices are not decreasing as they should in a stagnant economy where unemployment and poverty are increasing. The net result is that food and beverage businesses are forced to rethink product portfolios, costing and price points.

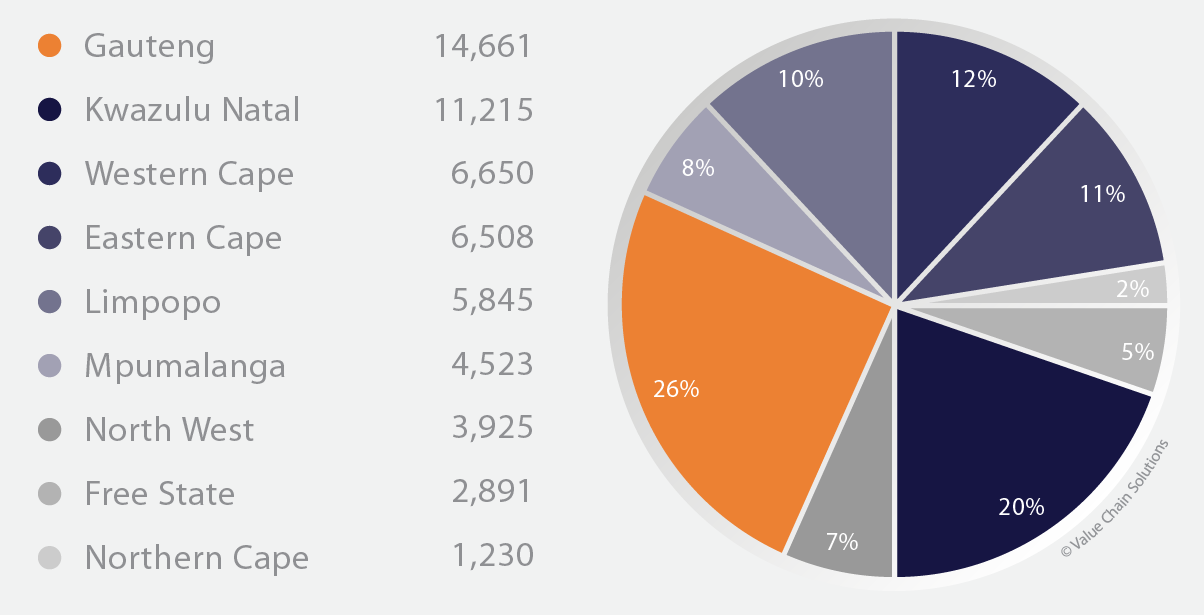

The South African population is a dichotomy of rural and urban-based people (Table 1). On the one hand, a large section of the population resides in urban areas such as Gauteng and eThekwini (Durban Metro). On the other hand, a significant section of the population resides in the rural areas of provinces such as KwaZulu-Natal, Eastern Cape, Mpumalanga and Limpopo.

Table 1. Source: StatsSA General Household Survey 2018

The net result, from a consumer perspective, is a strong section of the consumer base being highly urbanised and concentrated in urban centres, whilst another significant section is widespread in rural areas and much less urbanised in terms of needs and consumption patterns. Businesses are therefore forced to create and deliver products at the right time, in the right place and at the right price to cater for both these realities – a daunting task at the very least just to maintain a competitive value chain. Certain impacts of COVID-19, namely people’s disposable income being under pressure and others losing their jobs, only exacerbate the challenge of providing consumers with affordable food and beverage products whilst still maintaining company profitability and hence sustainability. The expected impact on consumer spending patterns are depicted in Table 2.

In summary

South Africa has been battling to overcome the imbalances of the past in terms of a highly dichotomised economy. This characteristic creates challenges for any business involved in the food and beverage sectors that wants to scale its operations and expand its product offering. With the outbreak of COVID-19 and resulting implications still unfolding, it appears as if this characteristic of the economy and hence the consumer base is only to intensify. This implies businesses will have to simply think and work harder and smarter to redesign products and value chains to ensure products remain relevant to the broader consumer market – whilst remaining profitable for the business. Product portfolios will also have to be rationalised to ensure there is a focus on key and scarce resources where it matters most.

Table 2. Source: StatsSA General Household Survey 2018, LCS 2015, TransUnion Financial Hardship